BitMEX Alpha

Bitcoin’s Underperformance: Understanding Supply-Demand Dynamics

This year, Bitcoin has underperformed in comparison to virtually every major asset class. Heading into the final quarter of 2025, Bitcoin's performance has notably lagged behind gold, Nasdaq, S&P...

Resources

How to Add Trading Chart Indicators on BitMEX

Reading trading charts is a crucial skill for any trader looking to make profit. Adding technical indicators to trading charts can help identify the right time to place a...

BMEX Token

What is the BMEX Token and Its Benefits?

The BMEX Token: Your Key to a Better BitMEX Trading Experience

Ready to level up your trading game? The BMEX Token is more than just a token. It's your access...

Resources

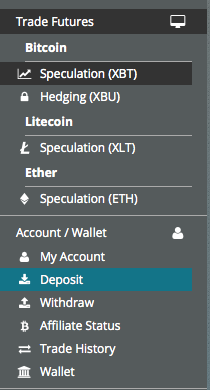

How to Place a Trade on BitMEX

Whether you are an experienced trader or new to the crypto space, understanding your platform is key to executing your trades. The difference between a profitable trade and a...

Resources

A Beginner’s Guide to Funding Your BitMEX Account

Funding your trading account is the essential first step to start trading crypto derivatives on BitMEX.

This article is a step-by-step guide on how to make a deposit on BitMEX ...

Resources

How to Create a BitMEX Account

Looking to get started with crypto derivatives trading on a safe crypto exchange? Below is a step-by-step guide on how to create and verify your account on BitMEX to...

Announcements

Now Live: Get Paid to Trade on BitMEX Spot

We are excited to announce a major upgrade to our fee structure for BitMEX Spot. We’re paying you to trade, and we’re slashing fees significantly to bring you the best fees in the market.

Listing

Now Live: Unlock DeFi Yield on BitMEX with Fija Finance

What if DeFi yields were accessible through the convenience of a centralised exchange but without the complexity of DeFi?

Introducing Fija Finance on BitMEX, a way to earn DeFi yield...

Announcements

API Update: Introducing the ‘strategy’ Field to the Order and Execution Endpoint

From 21 October 2025, a new field, strategy, will be added to the BitMEX Order and Execution table/endpoint.

BitMEX Alpha

Identifying Alpha Post-Meltdown: Are Bullbacks Still the New Pullbacks?

Explore the breakdown of the October 11 flash crash's systemic failures, the resilience of BitMEX, and the high-conviction narratives we have our eyes on as the primary targets for the next round of BTFD.

Pumping Iron

I used to be an amateur bodybuilder. Sometimes friends who haven’t seen me since university remark at how skinny I am...