Speculators care about obtaining exposure to risk. How they get that exposure if they can get in and out cheaply is secondary. If BitMEX is able to create a liquid market for Bitcoin quanto’ed derivatives, speculators will flock to them.

As I previously explained in “Why Quanto?”, in order for BitMEX to offer ETH/USD risk, we had to quanto into Bitcoin. This post will explore the concepts speculators care about.

For all the below examples we will use the following assumptions:

Contract: ETHUSD

Multiplier: 0.000001 XBT per 1 USD

Contracts: 10,000

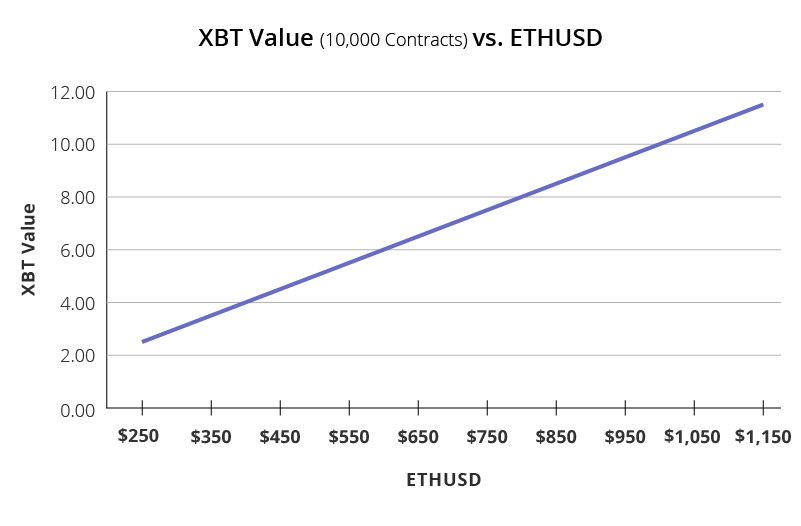

Contract Value

The most important aspect to a speculator is the contract’s payoff function. Since we are speculating on the ETH/USD price, ideally the contract’s Bitcoin value should increase and decrease in a linear fashion with respect to the ETH/USD price.

I assume the speculator denominates their profit in Bitcoin (XBT) terms. Therefore the value of Bitcoin in USD terms at a particular ETH/USD price is irrelevant. Put simply, the speculator wants to use Bitcoin as a margin to earn more Bitcoin.

The above chart illustrates that at different ETHUSD values, the XBT value of the position changes linearly. That is exactly what the speculator desires.

XBT Value = ETHUSD Price * Multiplier * # Contracts

Calculating Margin

How is the amount of Bitcoin margin calculated? The initial margin for the ETHUSD contract is 2%, or 50x leverage.

Initial Margin (IM) = 2% * XBT Value

If you enter the trade at an ETHUSD Price of $500, this is your initial margin requirement:

IM = 2% * $500 * 0.000001 XBT * 10,000 = 0.10 XBT

The next important consideration is what is your liquidation price. That is determined by the maintenance margin. The maintenance margin for the ETHUSD contract is 1%. If the underlying ETH/USD spot price declines by 1%, you will be liquidated.

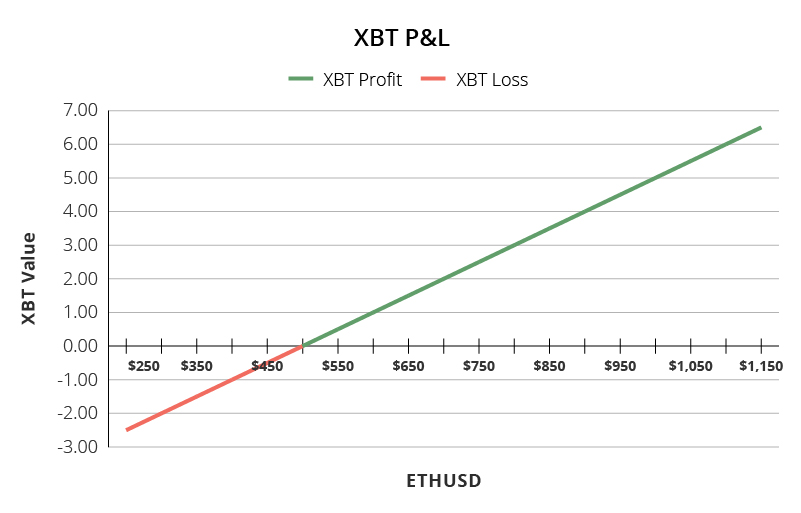

Calculating Profit and Loss (PNL)

The PNL is denominated in Bitcoin. In Bitcoin terms, the PNL changes linearly with the ETHUSD price. If the contract goes up 1%, your Bitcoin PNL also goes up 1%. The chart above illustrates that.

XBT PNL = (ETHUSD Exit Price - ETHUSD Entry Price) * Multiplier * # Contracts

In the above example, if the ETHUSD price moves from $500 to $600, this is the XBT PNL:

XBT PNL = ($600 - $500) * 0.000001 XBT * 10,000 = 1 XBT

Number of Contracts

To get a certain amount of Bitcoin exposure requires a little math.

The following describes how to calculate how many contracts it takes to equal a desired Bitcoin notional.

Contracts = XBT Notional / [ ETHUSD Price * Multiplier ]

If you want 100 XBT of risk, how many contracts of ETHUSD must you trade:

Contracts = 100 XBT / [ $500 * 0.000001 XBT ] = 200,000 Contracts

The quanto structure satisfies the desires of a Bitcoin-based speculator. The major components that speculators care about all vary linearly with respect to the ETH/USD price. The relative rich or cheapness of the contract vs. the underlying is not a major concern if the contract is liquid.

The factors that govern whether the contract will be at a premium or discount will be explored in the subsequent piece. These considerations heavily depend on how to hedge a quanto derivative from first principles. The hedging of the contract is where the non-linear effects matter.