(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Combining an acid with a base yields salt plus water. Chemistry 101. My high school chemistry teacher would be dismayed if he knew that’s all I remembered from his years of instruction.

Given the ingredients floating out there in the current global macro environment, the creation of Bitcoin was similarly inevitable – when you combine the internet, cryptography, and a decrepit and inequitable analogue financial system, you’re going to eventually pop out some sort of reactive technological development that attempts to ameliorate the disgusting status quo. Bitcoin and its blockchain happened to be the output.

And now you are off to the races. The permutations of ideas that sprouted from our Lord Satoshi’s white paper allows me to write every fortnight about new, interesting facets of the crypto ecosystem. DeFi, NFTs, The Metaverse, DAOs, and the decentralisation of everything are all the result of reactions between a number of naturally-occurring inputs – with the two most important ingredients being Bitcoin and an analogue system deserving of an upgrade to mesh with the age of the computer and internet.

While we revel in the BOOLMARKET of everything crypto, we must not forget the macroeconomic environment that provides a fertile substrate for the reactions driving our technological advancement. The orgy of post-COVID money printing and stimulus is giving even the most ardent supporters of command-and-control fiscal and monetary policies pause. The inflationary impacts of these policies across the most important manifestations of energy (food, housing, and transportation) are visibly destabilising the global social fabric.

They call it “transitory”, but they know the guillotine is quite permanent. Let them eat cake.

The debate amongst the high mandarin global clergy is whether enough is enough. While a vocal and powerful few greatly benefited from the global liquidity injections, the potential costs of a revolution – driven by those who work harder for less benefit – are too great to ignore. And thus, as we steam into Q4, the question becomes: how do we safely handle the hangover that will inevitably follow the tapering of monetary and fiscal stimulus?

This fortnight I shall take a break from my gushing admiration of the burgeoning Metaverse and return to macro basics. The question I will strive to answer is whether a reduction of the pace of money printing could cause headwinds for our crypto holdings. Maybe the groundswell of interest from those fed up with being financial serfs of TradFi can overcome less accommodative monetary policy and continue to drive crypto gains, but I would not make that assumption lightly.

Coffee Time

Luckily for the readers of this missive, I recently chatted with my favorite volatility hedge fund manager at a new coffee shop. This is the same bloke who inspired my “Pumping Iron” essay. I will refer to him as Jessie. (Bonus points if you can tell me why I chose that given name). Our usual spot was recently forced to shutter its doors, falling victim to yet another round of COVID lockdown measures. The new one, thankfully, is just right next door. They both serve below-average coffee aimed at a proletariat white collar workforce seeking stimulation to deliver them from their abject boredom in service to the Man.

As I alluded to earlier, I entered this meeting with a fear that I was underappreciating the risk that central bankers were actually serious about fighting the inflation they created by reducing bond purchases and raising short-term policy interest rates. My base case is that it is politically expedient for central banks to continue financing government stimulus programs by expanding their balance sheets. I also believe all major central banks have an unofficial mandate to make sure equity markets continue grinding higher. The inflationary pressures of these policies are a necessary evil, ensuring that domestic spending agendas can be paid for with rising asset prices. Stopping the money printer would decapitate asset prices, and render many financial institutions and governments insolvent. Therefore, it simply can’t happen– or so I believe.

Mark Twain said it best, “It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

With that in mind, I walked into this coffee meeting ready to test my view of the world with someone more intelligent than myself. I emerged even more bullish on crypto, and confident that the powers that be are not at all ready to endure the post-quantitative easing hangover. Over the next few thousand words, I will recount our conversation and annotate salient points with some chart porn.

Boomerang

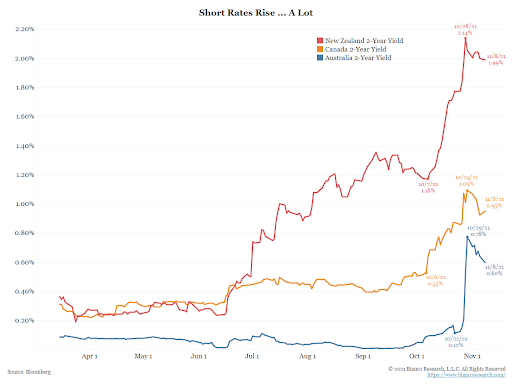

I opened our conversation by inquiring about his thoughts on the recent movement in Aussie rates. In the Land Down Under, the Reserve Bank of Australia (RBA) previously pledged to cap the 2 year-yield at 0.10% (which was textbook yield curve control, or “YCC”) and every time the market got a bit uppity, they would slam it down by purchasing enough bonds to reduce the yield at or below 0.10%. But recently the RBA decided they would no longer stifle price discovery for 2-year bonds.

The above chart – and the face-ripping rally in yields it depicts – clearly illustrates what happens when you remove the jackboot of central bank bond market purchases from the market’s bodice (not pictured: the plummeting bond prices driven by the spike in yield).

Anyone who shrugs their shoulders at a jump from 0.10% yields to 0.80% yields needs a primer in the total return math of bonds. That is an 8x increase in yield over the span of a few trading days. The move carried out many masters of the universe working at big name hedge funds. Jessie proceeded to tick off the names of a few large hedge funds whose credit desk got a tap on the shoulder. Thankfully for everyone, hedge funds can only really lose their clients’ money. If this were a Too Big To Fail bank’s trading desk, they would come hat in hand to the government and get a bailout … ‘cause “market stability”. Don’t you just love privatised gains and socialised losses?

I then asked Jessie why he thought the RBA let the market reprice the curve, especially since the RBA owns almost 70% of the supply of 2-year government bonds. They literally ARE the market.

He and I agreed on the why, and that was housing inflation. Let me explain.

I have a lot of Aussie mates. We often talk about the white-hot Aussie property market. The Aussie housing market has not experienced a real business cycle in modern history, meaning it has not experienced the significant correction in housing prices that usually accompany a real business cycle. The median house price to median salary ratio in Sydney and Melbourne is one of the highest in the world (the higher the ratio, the more unaffordable housing is).

The RBA takes a lot of political heat from their citizens about how unaffordable it is to own a house. For an economy that exports many of the raw materials that power our global economy (as well as tasty foodstuffs), their monetary policy is extremely accommodative. At some point, the inflationary pressures of holding rates well below nominal growth became too much, and the RBA bailed.

The question for the rest of the world is if and when similar decisions will be made in the major money printing centers of the US, EU, Japan, and China. Keeping this question in mind, Jessie had thoughts on the path the real players aim to take in the near future.

Butterfly Effects

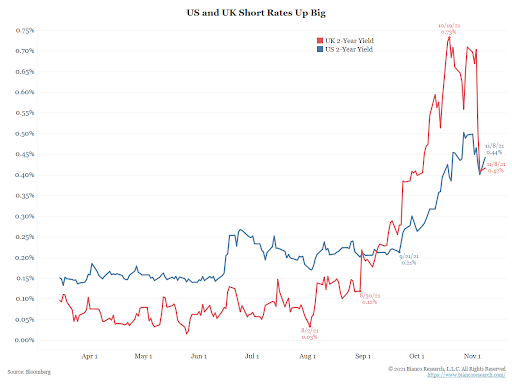

The Aussie rates flare-up acted as a catalyst for similar moves in other rates markets around the world. Every single major economy, regardless of their economic model, is rigging their government bond markets. Therefore, all central banks must toe the line – otherwise, the market might overwhelm the perceived control of central banks. That was the view shared by Jessie as he ticked off a few rates markets in which he was able to monetise a dramatic shift higher in short-term rates’ implied volatility.

My boy Jim Bianco of Bianco Research produces some awesome charts that demonstrate how the market has begun to put central bankers to the test. You wouldn’t know it from his appearance and age, but Jim is a shitcoiner and believes in the promise of DeFi. Mad respect.

In order to maintain the con of central bank omnipotence, any central banker that steps out of line and attempts to normalise inflation-fighting monetary policy must be dealt with. These flare-ups in the 2-year rates markets cannot be allowed to continue. Therefore, it’s time for the wayward central bankers to find religion again. It is unacceptable to allow the market to properly signal the inflationary pressures embedded in various domestic economies.

Make it Stop

The only thing that stops central bankers and politicians from continuing a policy of wanton money printing is inflation. And it’s not the inflation defined by government-produced, hedonically-adjusted inflation statistics. It’s the inflation that brings the people out into the street. It’s the inflation that prevents the average worker from being able to afford bread, milk, sugar, rice, rent, fuel etc. It’s the inflation that leaves you hungry after busting your ass as an “essential worker”.

If central bankers wish to continue printing money, they must convince the market that, should inflation appear, they will fight it by reducing bond purchases and raising short-term policy rates. That way, the market won’t freak out and dump their government bonds. However, the central bank also has to convince the populace that the obvious food, housing, and transportation inflation they are experiencing on a daily basis is not permanent, and is all part of a healthy and growing economy. That way, the populace refrains from expressing their discontent at the ballot box, or worse– in the streets.

When we got to this part of the conversation, Jessie rattled off a number of central banks who– prior to the most recent G20 shindig– committed their bank to drastically reducing bond purchases and/or raising rates, but have since doubled down on a policy of QE and zero percent interest rates after getting a good talking to by their betters. The most salient example cited was the BOE.

Pre-G20

Interest rate drumbeat grows louder as BoE governor warns it may ‘have to act’ over inflation

Post G20

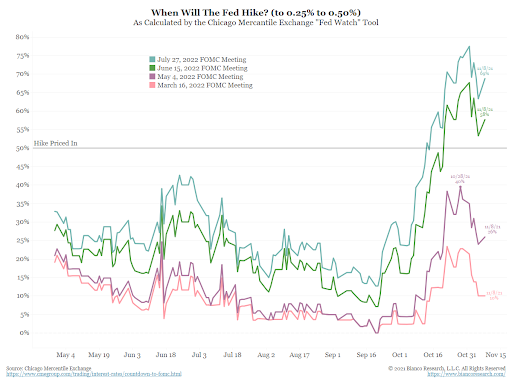

After digesting that, my next question was, “what will the Fed do?” Everyone else is just a two-bit player in this global central banking orchestra. The Fed is a violinist, errbody else plays the viola. (The viola … who the fuck plays the viola?)

Some more Bianco chart porn:

At its most recent meeting, the Fed initiated the “Taper”. It will begin reducing the amount of money it prints each month from now until June next year. At that point, the bond buying orgy stops, and the market believes they will then raise policy rates above zero.

The market might believe the Fed will begin raising rates in June 2022. But Jessie is of the view that if the Fed can get away with keeping rates at zero with little-to-no consequences, they will. Why would they remove the punch bowl before they absolutely have to? Every time they tried post-2008 resulted in a nasty correction in the equity markets. The taper tantrum of 2013 and the attempt to signal a resumption of interest rate hikes in 2018 are two prime examples of the dilemma facing the Fed and their global brethren.

June is awfully close to the most important month in America– November. In November 2022, US mid-term elections occur. The populace always votes with their wallets, and the ruling party receives either a vote of confidence or an early rebuke before the next presidential election in 2024. These days, their wallets are able to purchase less and less energy. The only way to stop this downtrend is if wages rise at the same pace as the cost of energy one consumes. The inflation tax doesn’t work if wages rise at the same pace as the growth in the money supply. Therefore, everything is done to convince the average worker that there is no inflation, and that their wages are sufficient to enjoy a happy life. If they are not convinced, they might organise themselves and decide to strike for higher wages.

Just like any organism, a politician is concerned first and foremost about survival. Inflationary policies line the pockets of the organisations and wealthy individuals that support their campaigns. The wealthiest 10% of Americans own nearly 90% of all US stonks. But, if they are voted out of office because the people don’t believe the “inflation is transitory” message, then they will throw the central bank under the bus and attempt to rein in inflation. The central bank is thrown under the bus if they are forced, due to political expediency, to turn off the money printer and allow the markets to reflect the true cost of money.

Even though the pace of bond buying will slacken, from now until the Fed June 2022 meeting, it’s motherfucking game on. The only thing not to own with 100% certainty are fixed income instruments.

What data point could prove me wrong? The real (unofficial) mandate of the Fed is to ensure a high and rising S&P 500 index. Like it or not, it is the yardstick everyone – rich or poor – looks to as the bellwether for the health of the American economy. And the higher it goes, the richer people feel, the more they spend, the more economic activity is generated, and the more tax dollars are collected. That’s the orthodoxy. It’s irrelevant if this logic is accurate, because the important people believe it to be true.

If the S&P 500 meltup halts and the index rediscovers gravity, that means the tapering of bond purchases is negatively impacting risky asset markets. That is a sign that a nasty correction in all risk assets might commence. The only thing that does well in that environment is long USD, as all manner of individuals and institutions sell risky assets to raise dollars to repay debt. That doesn’t necessarily mean crypto will be negatively impacted, but it would be a sign to tread carefully.

Smoke Alarms

Bitcoin and the broader crypto ecosystem provide two useful services to humanity. Firstly, they offer a different way to organise and incentivise humans in a decentralised fashion through superior technology. And secondly, they act as the only working smoke alarm in the global financial system.

If government bonds provided a real positive yield that compensated holders for inflation and future growth, there would be no reason to use bitcoin and other cryptos as an inflation hedge. Cryptos would only trade on the basis of whether a particular project could provide useful and transformative technology to humanity. Unfortunately (or fortunately, depending on the heaviness of your bags), a majority of shitcoins out there are just liquidity sucks. They pump because the temporal value of money has been so greatly perverted, it makes no difference whether you invest in dog money or a productive enterprise. In fact, it makes more sense to buy dog money because at least it is a liquid market that trades 24/7. Investments in actual businesses that produce good for humanity are illiquid, hard to value, and available to only a select few.

And so, as we close 2021, I remain cautiously bullish that the substrate of central bank money printing will continue to foster sick gainz for all manner of crypto assets. Thank you Jessie for shitty coffee, great conversation, and providing me with the intellectual pillars to reaffirm my faith in Lord Satoshi and all his angels.

I will leave you with my feelings on the major asset classes in which investors can plow their spare ducats:

Equities – oh yeah, gimme some S&P 500. Don’t got no positive earnings … don’t give a fuck. As long as I can buy it on Robinhood– preferably using out-of-the-money call options– my body is ready.

Real estate – please let me get a mortgage with 0% down payment, because my job does not let me afford to buy the median house. And if I don’t own my primary dwelling, rent will eat up 75% of my disposable income. Please oh please, private equity firms, don’t buy up all the single family houses and multifamily units in cash. I can’t afford to compete with you.

Crypto – fuck yeah baby! I want DOGEBONK, SHIB, FLOKI and any other meme coin. I want to be so crypto rich, I can tell my Dilbert-esque boss to go do one. And then I can become a digital nomad, move to Tulum, and vibe with Solomun on the weekends.

Bonds – ewwww those are for like … no one. No one should own these things. The central banks want them, they can have them.