(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Want More? Follow the Author on Instagram and X

PvP, or “player vs. player,” is a phrase used often by shitcoin traders to describe this current market cycle. The sentiment it evokes is predatory, where winning comes at the expense of others. That is so TradFi. The express purpose of the crypto capital markets is to allow those who risk their precious capital to enjoy the fruits of being “early” into projects that hopefully will grow apace with Web3. But oh, how we have strayed from the enlightened path laid down for us by Lord Satoshi and then subsequently Archangel Vitalik with his very successful Ether initial coin offering (ICO).

The current crypto bull market visited Bitcoin, Ether, and Solana big time. However, new issues, which I will define as tokens launched this year, have fared poorly for retail. The same can not be said for venture capital (VC) firms. Hence, the PvP moniker is ascribed to this current cycle. The result has been the launch of a plethora of high, fully diluted value (FDV), but low circulating supply projects. Post-launch, the token prices sloshed down the toilet like a common piece of doo-doo.

While that is the sentiment, what does the data show? The clever analysts at Maelstrom did some digging to answer a few niggling questions:

- Is it worth paying listing fees to exchanges so your token has a better chance of pumping?

- Are projects launching at valuations that are too expensive?

After I delve into the data that answers those questions, I want to offer some unsolicited advice to projects waiting in the wings, hoping the markets will turn around so they can launch. To bolster my arguments, I want to highlight a project within the Maelstrom portfolio, Auki Labs, that bucked the trend. They didn’t have CEX on the first date. Instead, they listed a relatively low-FDV token starting on DEX. They want retail to make money with them as they are hopefully successful in their journey to build a real-time marketplace for spatial computing. They also abhor the egregious listing fees that the major exchanges charge and believe there is a better way to give more value to end users rather than to the other big bosses who live in my neighbourhood in Singapore.

The Sample Set

We looked at a sample of 103 projects listed in 2024 across the major shitcoin exchanges.

This by no means is the total universe of all projects listed in 2024, but it is a representative sample.

Pump Up the Jam!

This is a common refrain from founders on our advisory calls, “Can you help us get listed on a CEX? It will pump our token price.” Hmmm… I never fully believed this. I believe that creating a useful product or service with increasing numbers of paying customers is the secret sauce to a successful Web3 project. Granted, if you have a piece of shit project that has value only because Irene Zhao reposted your content, then yes, you need a CEX so that you can dump it on their retail users. This applies to most Web3 projects, but hopefully not Maelstrom-backed ones … Akshat, take note!

The return is the number of days post-listing. LTD refers to live to date.

Regardless of the exchange, tokens have not pumped. If you paid exchange listing fees hoping for an up and to the right chart, soz.

Who won? The VCs won as the median token was up 31% over the last private round’s FDV. I refer to that as the VC Extraction Price. I will expound on the warped VC incentive structure that pushes projects to delay a liquidity event as long as possible later in this essay. But for now, most of you are just pure chumps! That’s why those dranks were free at the conference networking event … lolz.

Now, I’m going to get a little spicy. First off, CZ is a crypto hero for suffering at the hands of the TradFi devil in a medium-security US prison. I love CZ and respect his hustle and ability to move money from all sectors of the crypto capital markets into his pockets. But … But … trading an arm and a leg for a Binance listing ain’t worth it. To clarify, a primary listing where Binance is the first-ever exchange where your token is listed is not worth it. If Binance lists your token as a secondary listing because of your project’s traction and engaged community for free, that is definitely worth it.

Founders also ask on our calls, “Do you have a relationship with Binance? We MUST have a listing there; otherwise, our token won’t go up.” This Binance or nothing sentiment is very good for … Binance, which can charge the highest all-in listing fee of any exchange.

Referring back to the above table, Binance listed tokens may have outperformed the other major exchanges on a relative basis, but on an absolute basis the tokens prices still slumped. Therefore, a Binance listing does not guarantee rising token price.

A project must give or sell tokens, which are usually in finite supply, cheaply, to the exchange in exchange for a listing. Some exchanges are allowed to invest at an extremely low FDV regardless of the current last private round FDV. These are tokens that could have been given out to users for completing actions that promote the growth of the project. An easy example of a productive way to use tokens is how trading-focused apps emit tokens as a reward for traders hitting certain volume metrics, aka liquidity mining.

Selling tokens to a listing exchange can only be done once, but the positive flywheel of increased user engagement pays continuous dividends. Therefore, if you give up precious tokens just to get listed and only outperform a few percentage points on a relative basis, you are squandering precious resources as a project founder.

The Price Ain’t Right

As I tell Akshat and his team constantly, you have a job at Maelstrom because I believe you can compile a portfolio of the best-in-class Web3 projects that will outperform my core holdings of Bitcoin and Ether. If that weren’t the case, I would continue buying Bitcoin and Ether with my spare cash and not pay salaries and bonuses. As you can see here, if you bought a token at or around the listing price, you have underperformed the hardest money ever known, Bitcoin, and the top two decentralised computer layer-1’s, Ether and Solana. Given these results, retail should never buy a newly listed token. If you want crypto exposure, just stick with Bitcoin, Ether, and Solana.

This tells us that projects must cut their valuations at launch by 40% to 50% to become attractive on a relative basis. Who loses if tokens list lower prices, VCs and CEXs.

While you might believe that VCs are in the game to generate positive returns, the most successful managers realise they are in the asset accumulation game. If you can charge a management fee, usually 2%, on a large notional, you make money regardless of whether your investments appreciated in value. If you invest, as VCs do, in illiquid assets like early-stage token projects, which are just future token promissory notes, then how do you get the value to rise? You convince the founders to continue doing private rounds at ever-increasing FDVs.

As the FDV in private rounds increases, VCs get to mark-to-market their illiquid portfolio up in value. This shows great unrealised returns, which allows the VC to raise the next fund based on stellar past performance. This enables the VC to charge the management fee at a higher fund value. Also, VCs do not get paid if they don’t deploy capital. That isn’t so easy when most VCs set up in Western jurisdictions are not allowed to buy liquid tokens. They can only invest in equity of some sort of management company that writes a side letter giving their investors token warrants in the project they develop. This is why Sale of Future Token (SAFT) agreements exist. If you want VC money, and they have a fuck ton of dry powder, you must play this game.

What is toxic for many VCs is a liquidity event. When that happens, gravity takes hold, and token values plummet back to reality. The reality for most projects is that they have failed to create a product or service for which enough users will pay real money, which justifies their ridiculously high FDV. Now, the VC must mark their book lower, negatively impacting reported returns and the size of its management fee. Therefore, VCs will push founders to forestall the token launch as long as possible and continue doing private up-rounds. The net effect is that when the project eventually lists, it drops like a stone, as we have just witnessed.

Before I finish shitting on VCs, let’s discuss the anchoring effect. The human mind is very dumb sometimes. If a shitcoin opens for trading at a $10 billion FDV when it should be worth $100 million, you might dump the token and the net effect of all the sell pressure is the token drops by 90% to $1 billion and trading volume evaporates. The VC still gets to mark that illiquid shitcoin at a $1 billion FDV, which in most cases is well north of what they paid for it. Anchoring the market at an unrealistic FDV at open still pays off even if the price collapses.

The CEXs want a high FDV for two reasons. The first is that trading fees are charged as a percentage of the token notional. The higher the FDV, the more revenue and fees are earned, whether the project pumps or dumps. The second reason is that a high FDV and low circulating supply are good for exchanges because plenty of unallocated tokens can be given to them. The median percentage of circulating supply was 18.60% for the sample set.

Listing Fees

I want to talk briefly about the cost of listing on a CEX. The biggest issue with the current crop of token launches is that the price is too high. Therefore, it is almost impossible to have a good launch regardless of the CEX that wins the primary listing. If that weren’t bad enough, projects with too high of an initial price are paying an egregious amount of money in the form of project tokens and stablecoins for the privilege of listing a turd.

Before I comment on the fees, I want to emphasise that I see nothing wrong with CEXs charging listing fees. CEXs have spent much money gathering a user base, and it must be paid for. If you are a CEX investor or token holder, you should be delighted with their business acumen. But again, I am an advisor and holder of tokens; if my projects give tokens to CEXs rather than to users, it harms their future potential, negatively impacting how high their tokens can trade. Therefore, I want either founders to stop paying fees and focus on attracting more users or CEXs to dramatically lower their prices.

There are three main ways CEXs extract money from projects.

- They charge an outright listing fee.

- They require a deposit, that is returned if the project delists.

- They mandate a specific amount of on-platform project-financed marketing spend.

In general, every CEX’s listing team grades projects. The shittier your project, the higher the fee. As I always tell founders, if your project has few users then you need a CEX to dump your dog shit on the market. If your project has a product market fit and a healthy growing ecosystem of real users, you don’t need a CEX because your community will support your token price wherever it is listed.

Listing Fee

At the top end, Binance charges up to 8% of the total token supply as a listing fee. Most other CEXs charge between $250,000 and $500,000, paid in stablecoins.

Deposit

Binance devised a genius strategy for requiring projects to purchase BNB and stake it as a deposit. When / if the project delists, the BNB is returned. Binance requires up to $5,000,000 worth of BNB to be purchased and staked as a deposit. Most other CEXs require a deposit of $250,000 to $500,000 in stables or that CEX’s token.

Marketing

Binance at the top end requires the projects to give away 8% of their token supply to Binance users via on-platform airdrops and other campaigns. The medium-expensive CEXs require a spending of up to 3% of the token supply. At the bottom end, CEXs require a marketing spend of $250,000 to $1 million paid in stables or project tokens.

Added together, getting listed on Binance could cost 16% of your token supply and a $5 million purchase of BNB. If Binance isn’t the primary exchange, a project will still face spending of almost $2 million worth of tokens or stablecoins.

For any CEX who challenges these numbers, I implore you to provide a transparent accounting of every single cost or mandated spend that your exchange requires to list a new token. I received these numbers from several projects that have evaluated the costs of all the major CEXs. The data may be out of date. I will reiterate that I believe the CEXs are doing nothing wrong. They have a valuable distribution channel and are maximising its value. My gripe is that the post-launch token performance isn’t sufficient to warrant project founders paying these fees.

My Advice

This game is straightforward, make sure your users/token holders get rich as your project becomes successful. I’m speaking directly to YOU, project founders.

If you must, only do a small private seed round so that you can create a product for a very limited use case. Then, list your token. Because your product is nowhere near finding true product market fit, the FDV should be very low. This signals a few things to your users. Firstly, it is risky, that is why they are getting in at such a low price. You will fuck shit up, and your users will stay with you because they paid a meagre price to put skin in the game. But they believe in you, and you will figure it out given more time. Second, it shows that you want your users on a wealth-generation journey with you. This incentivises them to tell everyone about your product or service because users know there is a path for them to earn riches if more people join the movement.

Right now, many CEXs are under pressure, due to the severe underperformance of the vast majority of their new listings, to accept only “high quality” projects. Given how easy it is to fake it until you make it in crypto, it is very tough only to select the best projects. Garbage in, garbage out. Each major CEX has its preferred metrics, which it believes are leading indicators of success. Generally speaking, a super young project won’t meet their criteria. Fuck em, there is this thing called a decentralised exchange.

On a DEX, creating a new trading market is permissionless. Imagine you are a project that raised 1 million USDe (Ethena USD) and wants to offer 10% of your token supply to the market. You create a Uniswap liquidity pool comprised of 1 million USDe vs. 10% of your token supply. Click the button and let the automated market maker respond to the demand for your token in the market and set the clearing price. You do not need to pay any fees to do this. Now, your dedicated users can purchase your token instantly, and if you truly have an engaged community, the price will rise quickly.

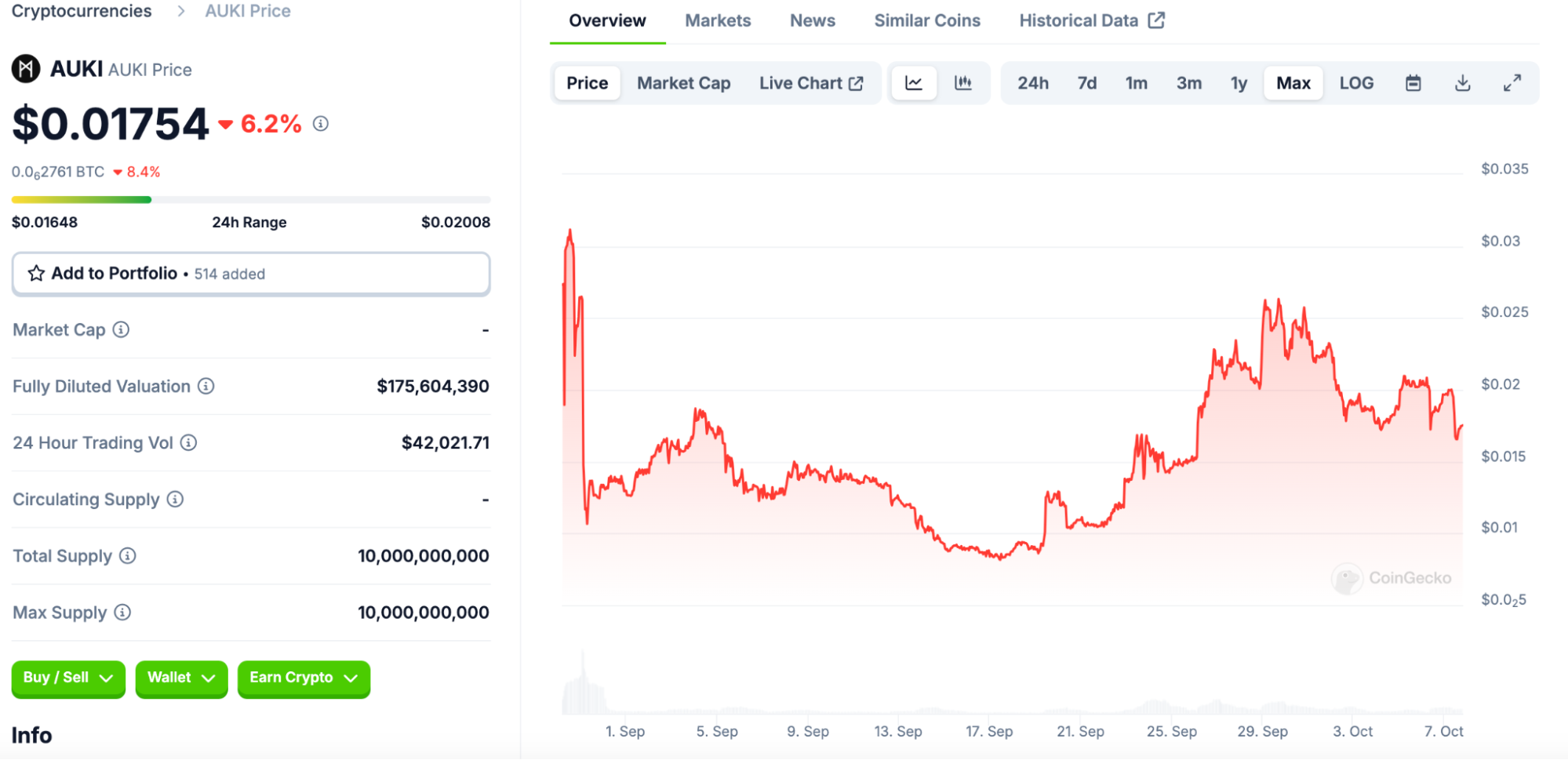

Auki Labs

Let’s step through how Auki Labs did something different when it came to launching their token. The above is a screen grab from CoinGecko. As you can see, the FDV and 24-hour trading volume are quite low. That is because it is listed on DEXs first and just followed up with a MEXC CEX listing. To date, Auki is up 78% over its last private round’s price.

To the Auki founders, the token listing was just another day. Building their product is their real focus. The token was listed on Uniswap V3 first via an AUKI/ETH trading pair on Base, Coinbase’s Layer-2 solution, on August 28th. Subsequently, they listed on their first CEX, MEXC, on September 4th. They estimate they have saved $200,000 in listing fees by going this route.

The Auki token vesting schedule is also more egalitarian. Team members and investors are on a daily vesting schedule with terms of one to four years.

Sour Grapes

Some readers might respond that I’m just salty that I don’t own one of the dominant CEXs printing money via new token listings. That is true; I make money based on the tokens in my portfolio increasing in value.

If projects in my portfolio are pricing their tokens too richly, paying massive fees to list on an exchange, and not outperforming Bitcoin, Ether, and Solana, I owe it to myself to say something. That is my angle. If a CEX lists a Maelstrom project because it has strong user growth and offers a compelling product or service, I’m all for it. But I want projects that we back to stop worrying about which CEX will take them and start worrying about their fucking Daily Active User count.