(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

The economics of nightclubs and national banking systems have a lot in common.

Patronising a nightclub is a lot of fun. You get to listen to good music, hang out with your friends, and for some, find a mate. However, after all the fun is had, there is always a bill to pay – and sometimes it can be quite substantial. Absent an agreed upon set of rules on how the cost should be allocated, the conversation as to who pays and how much can get quite heated.

“I was only there for a little bit.”

“I only had one drink.”

“I didn’t bring any girls to the table.”

Your scrub friend (you know the one) will always use excuses to avoid being part of the denominator of people who must split the bill. Early on in my banking career, my tight group of friends (we call ourselves the Fam) had a chat one day at work to codify the “bottle rules.”

The bottle rules determined whether or not a member of the crew was a part of the denominator and thus had to pay an equal share of that night’s bill.

The rules were simple:

- Girls don’t pay.

- If you have one drink, you are in for the whole bottle.

- If you bring one girl to the table and she drinks, you are in for the whole bottle.

- If you bring a friend who is male, and he has one drink, he is in for the whole bottle and you pay his share.

- If you order champagne, you pay for that entirely by yourself. This rule is crucial. There is one member of the Fam whose ego always gets ahead of his willingness to pay on various occasions. One time a few years ago at 1 Oak in Tokyo, he got the maths wrong and thought a train of 6 bottles of Dom P could be had for the price of one. He ordered the train, felt like a baller, and then – after realising his maths error when presented with the bill – tried to charge the entire group for his folly. He got a stern rebuke from another friend and paid for it entirely on his own in the end.

- If you order a bottle at the end of the night right before the club closes, you pay for that entirely on your own. (The same champagne friend is frequently guilty of this infraction, too.)

And now to the more pressing issue of how banking systems allocate inevitable losses.

Nations love robust banking systems. A good banking system allows the savings of the citizens to be aggregated and lent out to the government and productive companies. In an ideal world, this lending creates economic growth.

However, banking systems get into trouble quite often because they are fractionally reserved – i.e., they lend out more than they have on deposit. Their willingness to lend out money they don’t have frequently lands them in situations where they are unable to fulfil all of their depositors’ withdrawal requests, particularly during times of stress. These situations usually arise after some combination of political pressure, profit motives, and/ or poor risk management cause the banks to suffer massive losses, typically stemming from poorly underwritten loans or loan losses driven by rising interest rates. A bank run ensues, and then the government has to decide who is responsible for paying the bill to drag its glorious banking system back into solvency.

Should some combination of depositors, shareholders, or bondholders bear the cost of bailing out the bank? Or, should the government print money to “save” the defunct bank and pass on the cost to the entire citizenry in the form of inflation?

The most well-run banking systems establish an agreed upon set of rules governing these types of situations before any crisis occurs, ensuring that everyone knows how a failed bank will be dealt with, eliminating any surprises. Because banking systems are believed by the financial and political elite to be so integral to a well-functioning nation state, it’s safe to assume that in almost every country, banks will always be bailed out. The real question becomes, which schmucks get included in the denominator responsible for paying to recapitalise the bank? Regardless of what division of costs has been agreed to prior to any bank failure, once a bank actually collapses, every stakeholder involved will always lobby the government to avoid being part of the denominator.

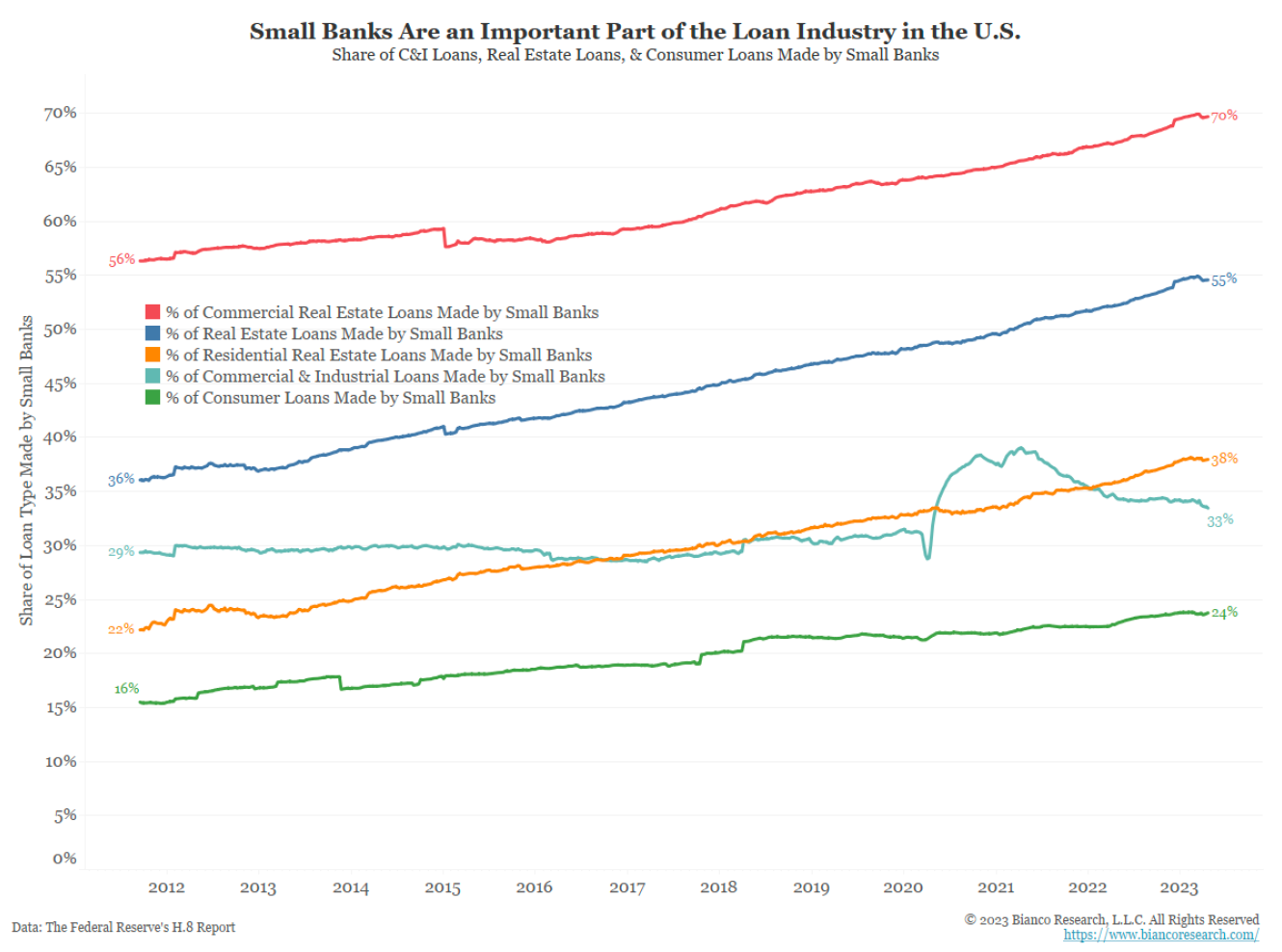

Bianco Research published a truly epic chart pack clearly illustrating the current and future disaster that is the US banking system. A few of their charts will be presented in this essay.

United States of America or United States of China

The US government is at a crossroads and has so far been indecisive about the kind of banking system it wants for Pax Americana. Does it want a decentralised system of small- to medium-sized banks who lend locally (i.e., the US banking system pre-2008)? Or does it want a centralised system of a few mega banks who primarily lend to the national champions, super-duper rich people, and Jeffrey Epstein (i.e., the Chinese banking system)?

Post the 2008 Global Financial Crisis, the pencil pushers in charge of banking regulations decided that they would create a two-tiered system. Eight banks were determined to be Too Big to Fail (TBTF) and given an unlimited government guarantee on their deposits.JP Morgan leads the pack, holding 16% of all US deposits. There is no risk in depositing to these mega banks. If a TBTF bank fucks up, the USG will print the money needed to make sure all depositors get their money back. Essentially, these 8 banks are state-owned enterprises for which the profits are privatised to shareholders, but the losses are socialised to the citizens. In return for this sweetheart deal, these eight banks were given a fuck-ton of new rules to follow. These mega banks then spent hundreds of millions of dollars on political campaign donations to help tweak those rules and achieve the most favourable set of restrictions possible.

Source: Open Secrets

Every other bank must weather the rough-and-tumble free market all on their own. All deposits are not guaranteed – and because of the risks involved, you would think that depositors should be clearly informed of exactly how these banks are lending out their money. Instead, depositors are left to decipher the banks’ purposely obtuse and misleading financial statements and arrive at their own conclusion regarding whether a given bank is well run.

All banks cater to different types of customers. The TBTF banks are geared towards servicing large corporations and super-rich individuals, and they are pros at securities lending and trading. TBTF banks are also conduits of the Federal Reserve (Fed) and US Treasury’s monetary policy, and they support the USG by buying lots of the country’s debt.

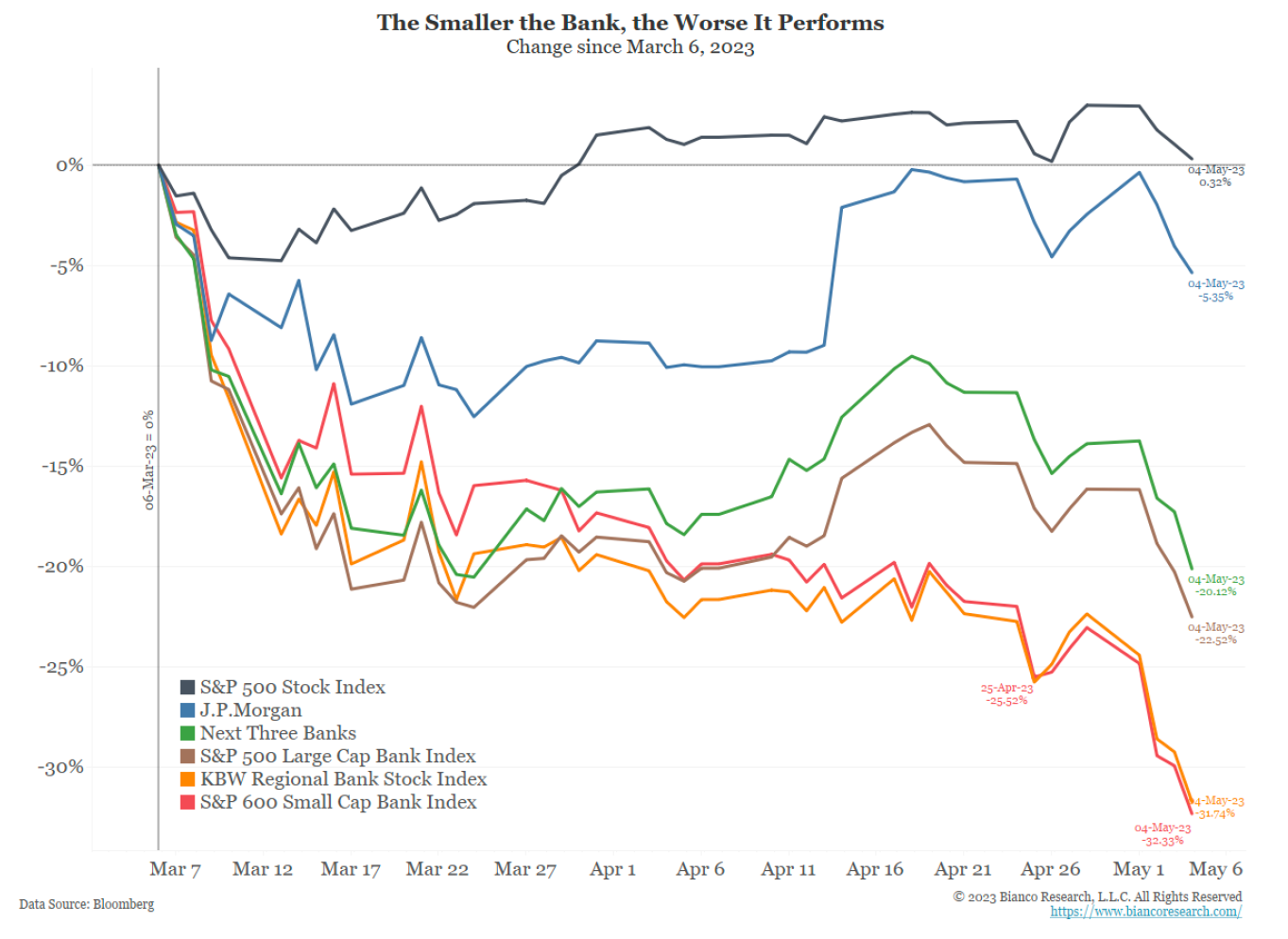

The non-TBTF banks, on the other hand, power the real engine of the US economy – that is, by providing loans to the small- to medium-sized businesses and loans to individuals of more modest means. They take the scraps the TBTF banks discard from the proverbial table, filling their loan books with commercial real estate, residential mortgages, car loans, and personal loans (just for example). Take a look at the next two charts that depict how integral a robust network of smaller non-TBTF banks are to the US economy.

While both cohorts of the US banking system are exposed to different types of credit risks via their respective loan books, they share the same interest rate risk. The interest rate risk is that if inflation rises and the Fed raises short term rates to fight it, the loans they underwrote at lower rates are worth less. That is just bond maths. (I discussed this phenomenon at length in my essay “Kaiseki”.)

When 3 banks failed within one week this March, the Fed and US Treasury hastily concocted a bailout scheme called The Bank Term Funding Program (BTFP). Under this plan, any bank that held US Treasury bonds (UST) or US Mortgage-Backed Securities (MBS) could give them to the Fed and receive 100% of their face value in newly printed USDs.

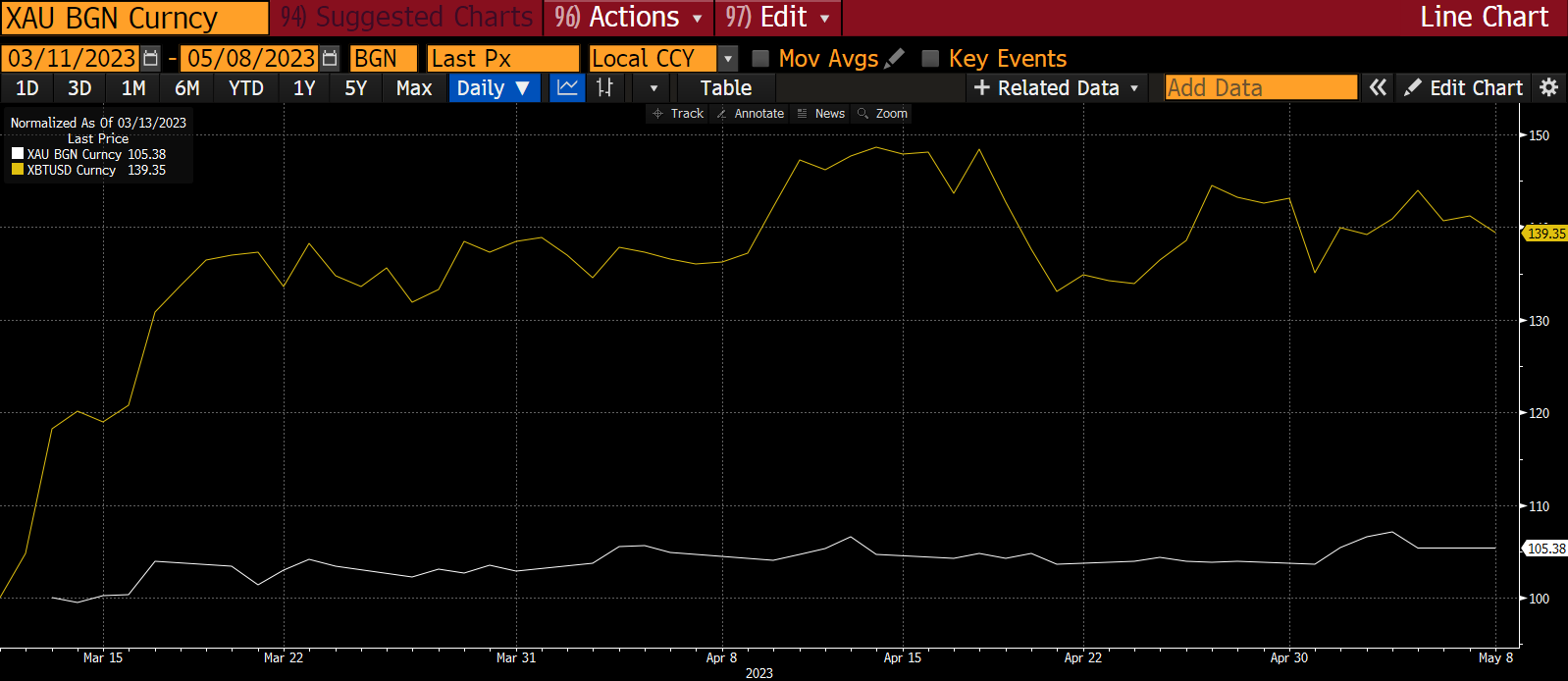

Given that the fiat-based fractional reserve banking system and the financial system of Pax Americana in general is a confidence game, the powers that be do not react kindly when the market calls bullshit on their antics. The financial markets rightly saw through the BTFP and recognised it as a thinly disguised way to print $4.4 trillion to “save” one portion of the US banking system. The market expressed its displeasure with this inflationary move by ramping the price of gold and Bitcoin. On the political front, various US elected officials did their best acting and cried foul at these banking bailouts. Con artists never like being called out, and the Fed & US Treasury realised that next time a bank(s) needed to get bailed out, it couldn’t be so obvious about what they were up to. That meant any tweaks made to the BTFP would need to be implemented surreptitiously. The tweak we are most interested in is related to the type of collateral that is eligible for the BTFP program.

From 11 March 2023 when the BTFP was announced, gold is up 5% (white) and Bitcoin is up 40% (yellow).

But first, it’s important that we understand what precipitated this tweak. The TBTF banks – as well as any bank that held a large percentage of its assets in UST or MBS securities – benefited from just the announcement of the BTFP. The market knew if and when these banks suffered deposit outflows, they could easily meet their cash needs by giving the eligible bonds to the Fed and getting back dollars. But the non-TBTF banks were not so lucky, because a large percentage of their assets were ineligible for BTFP funding.

In less than one financial quarter, the market saw through the BTFP and put stress on the non-TBTF banks. The market wondered, “who is going to pay the bill for the interest rate losses on their loan books if they can’t access the BTFP?” And that led them to ask themselves, “why would I own equity in a bank that can’t receive implicit or explicit support from the government?” That question is especially important as the recent First Republic bailout demonstrated that he “price” for the FDIC arranging a shotgun marriage between a failing non-TBTF bank and healthy TBTF bank is a complete wipeout of equity and bondholders. As a result, equity owners started dumping their stakes in the regional banks … a 99% loss is better than a 100% loss. Whoever sells first, sells best.

First Republic was the first post-BTFP casualty, and the way in which it was wound up gives us more clues as to who is in and who is out of favour with the USG. The politics of bank bailouts is toxic. Many plebes are pissed off that they lost their house, car, and/or small business in 2008, while the large banks got hundreds of billions of dollars-worth of support from the government and paid record bonuses. Therefore, politicians are loath to support optically obvious banking bailouts, especially since America is (in theory) a capitalist society where allowing companies to fail is supposed to be part of the system.

I’m sure US Treasury Secretary Janet Yellen got reamed out for the BTFP and was told that under no circumstances could the USG be seen bailing out additional failed banks. I imagine she was told the private market must find a solution for managing a non-TBTF bank failure – meaning that a tweak to the BTFP that would make any and all banking assets eligible for funding was off the table. A while back, US President Joe Biden told Jerome Powell – the Chairman of the Fed – that stopping inflation is his number one priority. Not wanting to go against the President’s wishes, the Fed could not lower interest rates enough to help stem the deposit outflow from these shaky banks while inflation was still at 5% (I will expand on this later in this essay). The two major financial arms of the government (Fed & US Treasury) could not alter their policies to effectively deal with this banking crisis for political reasons.

“I ran for president because I was tired of the so-called trickle-down economy. We now have a chance to build on a historic recovery with an economy that works for working families. The most important thing we can do now to transition from rapid recovery to stable, steady growth is to bring inflation down. That is why I have made tackling inflation my top economic priority.”

US President Joe Biden in a WSJ op-ed from May 2022

The Federal Deposit Insurance Corporation (FDIC), the US government body in charge of winding up failed banks, tried its best to bring together the TBTF banks to do their “duty” and purchase the loser banks. Unsurprisingly, these profit-motivated, government-backed enterprises wanted nothing to do with bailing out First Republic unless the government was willing to chip in even more. That is why, after many days and a stock price drop of 99%, the FDIC seized First Republic in order to sell its assets to meet depositor liabilities.

Note: A bank’s stock price is important for two reasons. First, a bank must have a minimum amount of equity capital to back its liabilities, aka skin in the game. If the stock price falls too far, then it will be in breach of these regulatory requirements. Second, a bank’s falling stock price prompts depositors to flee the bank for fear that where there’s smoke there’s fire.

In the 11th hour, just before markets opened on Monday 1 May 2023, the FDIC offered JPM, the largest TBTF bank, a sweetheart deal, and it agreed to purchase First Republic. The deal was so good that JPM CEO Jamie Dimon cooed on a shareholder call that the bank would recognise an immediate $2 billion profit. JPM, a bank with a government guarantee, refuses to buy a failed bank until the government gives it a deal so favourable that it makes $2 billion instantly. Where is Jamie’s patriotism?

Don’t let the numbers distract you from the important lesson of this bailout. The First Republic transaction illustrates the pre-conditions for getting nationalised via a purchase by a TBTF bank. Let’s walk through them.

Condition:

Equity holders and bond holders get wiped out. A donut … A bagel … A goose egg. Capeesh?

Response:

If your bank has interest losses on its loan portfolio (which every single bank has), and these loans are ineligible for the BTFP, you must sell that stock IMMEDIATELY! You don’t want to get deaded by the FDIC. Short sellers are not responsible for the collapse in these dogshit bank stocks. It is long holders selling for fear of a 100% loss of capital if and when the FDIC steps in.

Condition:

A TBTF bank with a government guarantee must purchase the failed bank by assuming its assets. The TBTF bank will only do this with additional government assistance provided by the FDIC.

Response:

In the First Republic situation, JPM got cheap loans from the FDIC, and the same agency bore 80% of any losses on the loan book. Essentially, it appears the government will only expand BTFP-eligible collateral if a TBTF bank buys a bankrupt bank first. This is clever, and most politicians and their constituents won’t realise that the USG expanded their support of the banking system without formally declaring it. Now the FDIC’s balance sheet will be bloated with potential losses from failed bank loan books and low interest loans to TBTF banks. Therefore, Powell, Yellen, and the Biden administration cannot be easily accused of printing money to bail out a bank.

The Critical Assumption

If you believe that, when push comes to shove, US policy makers will always do what it takes to save the banking system, then you must agree that all deposits in federally chartered banks will eventually be guaranteed. If you don’t agree, then you must believe that some bank depositors will suffer losses.

To assess which side is more likely to be true, look no further than the banks that have failed so far in 2023 and how they have been dealt with.

|

Bank |

Seized by FDIC |

Equity Holders |

Depositors |

|

Silvergate |

No |

Might get value from bankruptcy |

100% Made Whole |

|

Silicon Valley Bank |

Yes |

Wiped Out |

100% Made Whole |

|

Signature |

Yes |

Wiped Out |

100% Made Whole |

|

First Republic |

Yes |

Wiped Out |

100% Made Whole |

Note: Technically Silvergate was not seized by the FDIC as it declared bankruptcy before failing completely.

In all circumstances where the FDIC seized the bank, depositors were made whole. Thankfully Silvergate, even though it declared bankruptcy, was still able to make depositors whole as well. Therefore, even if you are in a non-TBTF bank your money is most likely safe. However, there is no guarantee that if the FDIC seizes the bank a TBTF bank will swoop in and make depositors whole; there is also no guarantee that if a bank declares bankruptcy it will have enough assets to fully cover all deposits. Therefore, it is in your best interest to move all your funds over the insured $250,000 limit to a TBTF bank who has a complete government deposit guarantee. This will inevitably drive large deposits from non-TBTF to TBTF banks and further exacerbate the issue of deposit flight.

The reason US Treasury Secretary Yellen cannot offer a blanket deposit guarantee to all banks is that it requires an act of the US Congress. And as I argued above, there is no appetite for more perceived banking bailouts by politicians.

Deposit Outflows

Non-TBTF banks will continue to lose deposits at an accelerating rate.

First, as I argued above, in order to be 100% sure your deposit is safe, you must move your money from a non-TBTF bank into a TBTF bank.

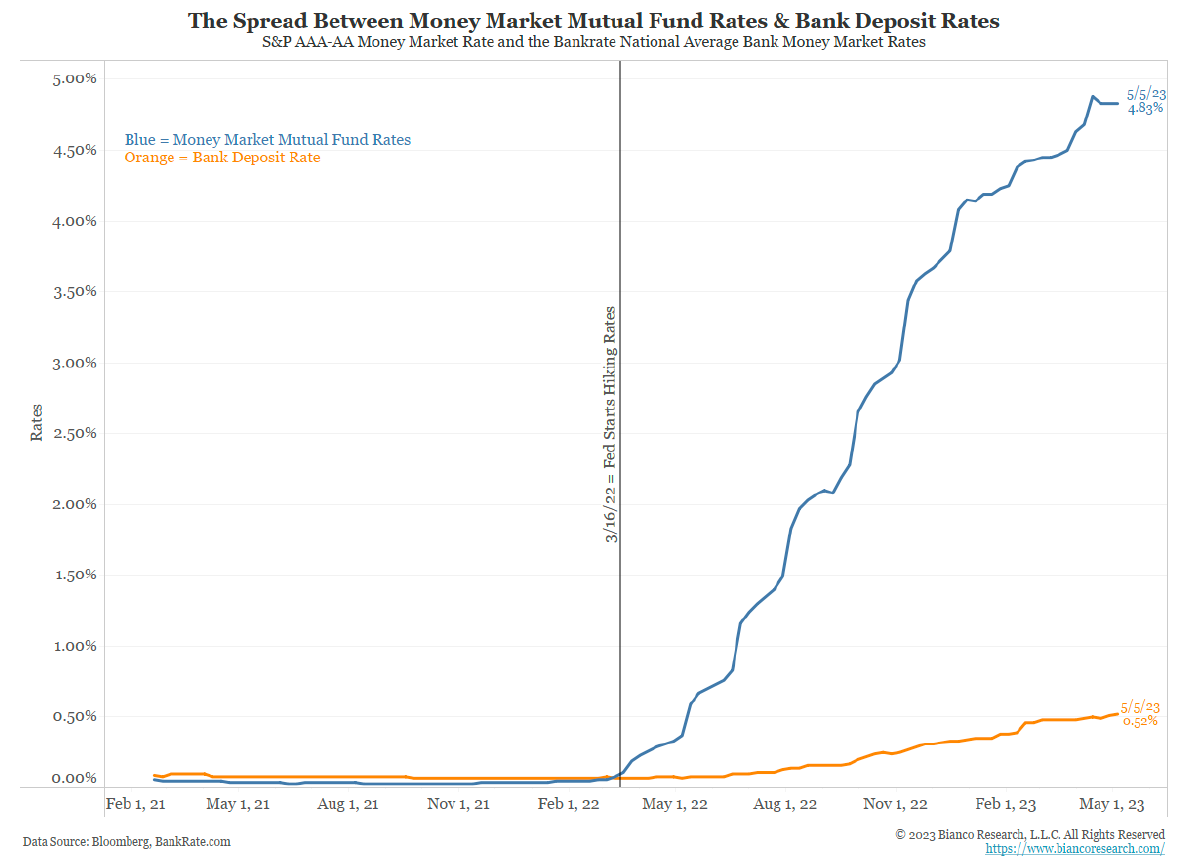

Second, all banks will lose deposits to money market funds, which deposit money with the Fed and/or invest in short-term US Treasury bills. Think about it – you can earn almost 5% in a money market fund, or 0.50% as a bank depositor (see the above chart). If you could move your money and almost 10x your interest income using your mobile phone within the time it takes to consume a few TikTok videos, why would you leave your money on deposit at a bank?

Even if you can’t be arsed to figure out what a money market fund is and want to just leave your money in the bank, there’s no reason to do it at a non-TBTF at this point. The TBTF banks can lose deposits and you don’t have to care, because at the end of the day, the USG explicitly guarantees you will always get your money back. Non-TBTF banks are just plain fucked, and deposit outflows will continue to drive failures.

If inflation, interest rates, and banking regulations remain as they are right now, there is no scenario where every single non-TBTF bank does not fail. There will be a 100% failure rate. Guaranteed!

Ok … maybe that’s a bit aggressive. The only banks that would survive are those that operate in a fully reserved model. That means they accept deposits, and immediately deposit those funds with the Fed on an overnight basis. This is a super safe way to do banking, but unfortunately the Fed no likey this type of banking. They have denied applications for banks wishing to employ this business model for unknown reasons.

The Denominator

If my prediction about the ultimate fate of all non-TBTF banks is correct, then how much larger can the US money supply get? That is the real question. With the BTFP, we know that the potential expansion is at least $4.4 trillion (i.e., the amount of UST and MBS on US banks’ balance sheets which can be exchanged for cash at any point).

We also now know that the preferred sleight of hand of the Fed, US Treasury, and banking regulators is to heavily insist that a TBTF bank assume the liabilities of a failed non-TBTF bank. The TBTF banks undertake this public service by receiving cheap capital and loss absorption paid for with government-printed and American taxpayer money. Therefore, the money supply will in essence be expanded by the total amount of loans of non-TBTF banks, which is $7.75 trillion.

Note for Ned Davis Research subscribers: I encourage you to look at the report ECON_51 to verify my $7.75 trillion number.

As a reminder, the reason why these loans must be backstopped is because deposits fled. As deposits flee, the bank must sell loans for much less than face value and realise a loss. The realisation of the loss means they fall below regulatory capital limits and, in the worst case, do not have enough cash left over to pay out depositors in full.

The only way all non-TBTF banks don’t go bankrupt is if one of the following things happens:

- The Fed cuts rates such that the yield of the reverse repo facility or three-month T-bills drops below the 2% to 3% range. The 2% to 3% range is an estimation of the blended yield of the banks’ loan portfolio. The Fed might cut rates either because inflation is falling, or they want to prevent further stress on the US banking system. Banks can then raise deposit rates to match or slightly exceed what money market funds can offer, and bank deposits will grow again.

- The BTFP eligible collateral is expanded to any loan on a US bank’s balance sheet.

Option 1 loosens financial conditions and risk assets like Bitcoin, gold, stocks, real estate, etc., all pump.

This is a decline in the price of money.

Option 2 enlarges the amount of money that will eventually be printed. And again, this is only supportive of risk assets that are outside of the banking system. That means that gold and Bitcoin pump, and stocks and property dump. Stocks drop because bank credit disappears and companies are unable to finance their operations. Property is outside of the financial system, but it is so expensive in nominal dollar terms that most buyers must finance purchases. If mortgage rates remain high, no one can afford the monthly payments, and prices fall.

This is an increase in the supply of money.

Either way, gold and Bitcoin are going up because either the supply of money increases, or the price of money decreases.

But what if the price of money continues to increase because inflation refuses to slacken and the Fed continues raising rates? Just last week, Sir Powell continued stressing that the Fed’s goal is to slay the inflationary beast, and he followed it up by raising rates by 0.25% in the midst of a banking crisis. In this case, non-TBTF banks will continue going bankrupt as the spread between money market funds and deposit rates grows which causes depositors to flee, and that results in bankruptcy eventually leading to their loans being backstopped by the government anyway. And as we know, the more loans the government guarantees, the more money must eventually be printed to cover losses.

The only way the money printer doesn’t go brrr is if the USG decides it will let the banking system actually fail – but I have full confidence that the US political elite would rather print money than right size the banking system.

Many readers might think to themselves that this banking issue is purely an American thing. And given that most readers are not citizens of Pax Americana, you may think this does not affect you. Wrong! Due to the USD’s reserve currency status, most nations import American monetary policy. More importantly, many non-US institutions such as sovereign wealth funds, central banks, and insurance companies own USD-denominated assets. Like it or not, the USD will continue to depreciate against hard assets like gold and Bitcoin, as well as useful commodities like oil and copper. You are in the denominator too, just like a red-blooded Jane Doe American schmuck.

Boom Boom Boom

If inflation stays high and the Fed continues raising rates – or even just keeps them where they are today – then more banks will fail, we’ll see more TBTF bailouts, and the government will continue to support the creation of larger and larger TBTF banks. This would expand the supply of money and gold, and Bitcoin would rally.

If inflation falls and the Fed cuts rates quickly, eventually, banks would stop failing. But, this would reduce the price of money, and gold and Bitcoin would rally.

Some may ask why I didn’t consider the outcome where the banks survive long enough for their low interest rate loans to mature, and be replaced by loans underwritten at a much higher yield. Depositors are not going to wait 12 to 24 months earning basically 0% at the bank vs. 5% in a money market fund. Tap tap, slide slide, and in less than 5 minutes your deposit base is gonzo, courtesy of your slick mobile banking app. There is just not enough time!

You just can’t lose owning gold and Bitcoin, unless you believe the political elite is willing to stomach a complete failure of the banking system. A true failure would mean that a large swath of chartered banks fold. This would stop any and all bank lending to businesses. Many businesses would fail, as they would be unable to finance their operations. New business creation would also decline in the absence of bank credit. House prices would plummet as mortgage rates spike. Stock prices would dump because many companies gorged on low-interest debt in 2020 and 2021, and when there is no longer affordable credit available to roll over their debt they would go bankrupt. Long-dated US Treasury bond yields would surge without the support of the commercial banking system buying bonds. If a politician reigned during a period in which these things happened, do you think they would get re-elected? No fucking chance! And therefore, while the various monetary authorities and banking regulators may talk a big game about no more bank bailouts, when the shit really hits the fan, they will dutifully press dat brrrr button.

Therefore, it’s Up Only! Just make sure you are not the last sucker in the Western financial system when the bill comes. Get your Bitcoin, and get out!