Abstract

We take a look at where we are in the Bitcoin mining cycle. We compare current market conditions to the gold mining industry in 2012 to 2014 and note the mad rush of capital flowing into the space. We project significant increases in both the network hashrate and financial failures in the mining space, over the coming years. We predict miners and products focusing on the long term, who deploy capital more conservatively across the cycle, may succeed.

Bull market

Bitcoin is trading over US$40,000 a coin, up from around US$5,000 a few years ago as the crypto space booms. Understandably many people are keen to get into the booming space, with a plan to launch a company and hopefully make a fortune. If you are not smart enough to launch a Defi DEX, there is one thing that seems far more simple, you can launch a new Bitcoin mine. What could be easier than that?

This brings me back to around 2012, with gold trading over US$1,600 a troy ounce. With the benefit of hindsight, this was the end of a 13 year bull market, which began at around US$250 an ounce in 1999. The move in the gold price, over six times and the success of the industry veterans, caused a frenetic rush of capital into the gold mining space. For those who remember the Prospectors & Developers Association of Canada (PDAC) conference in 2012 or 2013, it was quite an exciting time.

There were thousands of people looking to raise money for their prospective gold mine, all with remarkably similar stories and pitches:

- Two mates with an investment banking background (Co-founders of the mining company)

- One really smart geologist, working in an advisory capacity, who swears by the feasibility of the project

- An exceptionally high quality site in North America, with very strong grade, of over five grams per tonne

- It is open-pit only (An underground mine would have been too technically complicated)

- Mine will be ESG friendly and has strong local support (Founders have had beer with the locals)

- Reserves of around 500k troy ounces and annual production of 50k troy ounces

- Looking for an initial investment of US$50 million

- Chairman Bernanke only has one tool he is willing to use, money printing. Therefore the gold price is set to continue to increase

- In the long term, the company will scale up and become the next Goldcorp

Needless to say, not all of these potential projects raised the money they were looking for and for those that did, most failed to appreciate the challenges involved and the projects often failed. The equivalent pitch in Bitcoin is as follows:

- Two mates with an investment banking background (Co-founders of the mining company)

- One really smart Bitcoin guy who got into the space super early, working in an advisory capacity

- Looking to build a 50MW facility in North America, will will achieve one exahash of mining power per second

- Plan to go with Bitmain at the start, but open to others if it makes sense

- Mine will be fully ESG friendly (Carbon neutral company)

- Require initial funding of US$200 million

- It is inevitable that the Bitcoin price will continue to increase

- In the long term, to scale up and become the world’s largest Bitcoin miner

In some cases, we won’t mention any names, it is the same people who pitched gold mines in 2012, now jumping on the Bitcoin mine bandwagon. Many of these projects will end the same way as the gold projects 10 years earlier, in failure. Although a few may succeed.

Listed miners

Below is a list of Bitcoin miners, the lucky ones who made it to public markets. 21 miners with a combined market capitalisation of US$15.3 billion. The miners are at various stages, with Core Scientific (the largest) operating over 8 exahash of mining power per second, compared to Terawulf for example, that is just starting to ramp up production.

| # | Ticker | Name | Market Cap (US$ m) |

| 1 | CORZ US | CORE SCIENTIFIC | 2,637.5 |

| 2 | MARA US | MARATHON DIGITAL | 2,337.2 |

| 3 | RIOT US | RIOT BLOCKCHAIN | 1,956.1 |

| 4 | NB2 GR | NORTHERN DATA | 1,407.6 |

| 5 | CIFR US | CIPHER MINING | 865.6 |

| 6 | HUT CN | HUT 8 MINING | 796.2 |

| 7 | WULF US | TERAWULF | 793.5 |

| 8 | HIVE US | HIVE BLOCKCHAIN | 758.8 |

| 9 | IREN US | IRIS ENERGY | 752.3 |

| 10 | BITF US | BITFARMS | 640.0 |

| 11 | ARB LN | ARGO BLOCKCHAIN | 436.1 |

| 12 | CLSK US | CLEANSPARK | 431.7 |

| 13 | GREE US | GREENIDGE GENERATION | 353.2 |

| 14 | MIGI US | MAWSON INFRASTRUCTURE | 298.5 |

| 15 | SDIG US | STRONGHOLD | 237.3 |

| 16 | BTBT US | BIT DIGITAL | 209.6 |

| 17 | BTCM US | BIT MINING | 184.6 |

| 18 | DGHI CN | DIGIHOST TECHNOLOGY | 95.4 |

| 19 | DMGI CN | DMG BLOCKCHAIN SOLUTIONS | 83.6 |

| 20 | CBIT CV | CATHEDRA BITCOIN | 39.2 |

| 21 | CSTR CN | CRYPTOSTAR | 32.1 |

| Total | 15,346.0 |

Source: Bloomberg

Note: Market Cap as at 11 April 2022

We estimate that the above miners currently produce around 25% of the Bitcoin hashrate. The percentage of network hash rate controlled by public miners has been expanding rapidly over the last few years, as more names come to market, and due to access to capital, the listed miners have been expanding faster than their private peers. With Bitcoin above US$40,000, projected gross profit margins are very strong and one thing that is common across the 21 names above, is aggressive expansion plans. The large miners (at least the top 15), plan on each expanding by over 1 exahash in the next 12 months. Many of these large miners are building individual sites over 250MW and almost all operate in North America.

It is almost as if many of the listed miners are in a mad race to deploy capital first and achieve scale. They know access to capital is easy now, conditions which may not last forever and therefore if the miners do not spend now, they could fall behind their peers and never catch up. Now is the one chance to potentially become a CEO and large shareholder of a mega cap Bitcoin miner, they do not want to miss it. This feels just like the gold mining space in 2012 and it did not end well.

Based on current hashrate deployed, many of the above miners also look quite expensive, especially the ones who have emerged on public markets more recently and are only ramping up production, rather than actually mining now. There is considerable dispersion in valuation ratios, even when looking at relatively simple ratios such as market capitalisation to hashrate currently deployed. This may present an interesting opportunity to some investors or traders. Another interesting metric to look at is calculating the expected Bitcoin mined (based on reported hashrate) compared to reported Bitcoin mined. Some miners do not look too favourable based on this metric, while others are bang inline with expectations.

Miner equipment financing

In addition to equity financing, debt is also a popular model, often secured against mining machines. A new small miner can use a large hosting provider such as Core Scientific to host the machines and therefore all the operational issues can be dealt with by Core Scientific, all the miner needs to do is raise capital. This can make securing debt even easier, in the event of liquidation, ownership of the hardware can transfer to the creditor and the miner can continue to operate in the Core Scientific facility. As credit investors are keen to pour into the space, typical rates have come down to around 9% in Q1 2022 compared to 26% in early 2021. These rates are according to the CEO of Core Scientific, Mike Levitt, speaking at a recent side event at Bitcoin 2022 in Miami.

Galaxy Digital is the single largest lender to the miners. The lending team is headed up by Amanda Fabiano. She is regarded as extremely knowledgeable on miner financing and is sometimes called the “queen of mining lending”. We have also seen more traditional banks enter the miner lending space, adopting traditional equipment financing models, providing quite attractive terms to miners. These banks could lack the expertise of dedicated lenders in the field such as Amanda.

Royalties and Streaming

One model yet to gain any significant traction in Bitcoin miner financing is royalties and streaming. When this model is mentioned to some in the space, it is sometimes met with confusion and bewilderment. However, streaming is a common tool used by gold miners, often used alongside more traditional forms of financing like debt and equity.

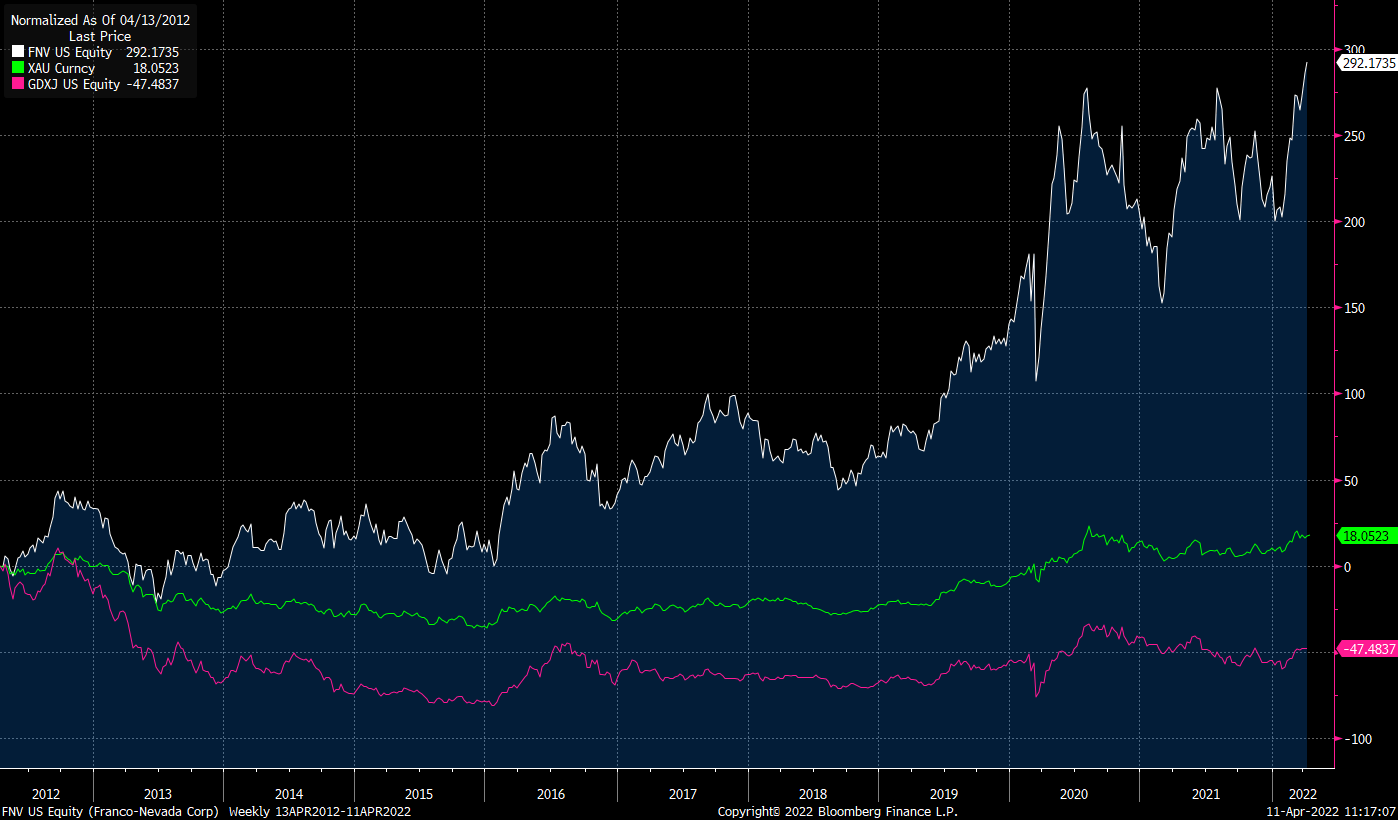

In gold mining, streaming has been the most successful model from an investor perspective. As the chart below illustrates, the largest gold streamer, Franco Nevada (blue), has outperformed both gold (green) and gold miners (pink). This is despite the fact that streaming has a considerably lower risk profile than mining.

Percentage returns since 2012 (In US$)

The streaming model works as follows: The steamer provides a cash lump sum upfront to the miner, in return the streamer is entitled to 5% of any gold produced by the mine, in perpetuity. There is no debt and therefore no possibility of default. If the mine is transferred to new ownership, the stream moves over. If the miner shuts down, the streamer has no earnings, but can patiently wait until the next gold bull market and the resumption of production. It is important that the steam percentage is low, perhaps 5% or less, or it may start to materially influence the economic decisions of the miner, who still retains the bulk of the economic output.

It is challenging to see how this model can be applied to Bitcoin mining, due to the lower expected economic life of the ASICs. On the other hand, as Bitcoin shot up to its all time high of US$68,991 in November 2021, Bitmain S9 machines, a machine released 4 to 5 years ago, many of which became idle, started to turn on again. This illustrates that ASICs may have a longer economic life than many expect and as the incremental improvements in efficiency get smaller, it is not too difficult to see that the streaming model, applied to particular ASICs, could work. We will not be surprised to see some of the current fleet of Whatsminer M30S+ machines operational in 10 or even 20 years time, in bull market periods. Therefore long term investment products, without an expiry date, may be attractive for some investors.

With no debt and no possibility of default, we will not be surprised if the streaming model begins to gain some traction in ASIC financing. Even if the model remains behind debt and equity as the primary financing models, it could be the model most attractive to investors and could be a good opportunity for an established or new mining financing company to facilitate. (e.g. Blockstream, Galaxy, Maple, Compass)

ASIC manufacturers

In the US, it looks like there are two dominant Chinese Bitcoin ASIC makers, Bitmain (Antminer) and MicroBT (Whatsminer) supplying all the equipment. However, the oldest ASIC maker, the Chinese company Canaan (Avalon), who produced their first machine in 2013, is very much still in the game globally and making a bit of a comeback. Globally, Canaan is actually pretty close to MicroBT in terms of market share. Canaan has a leading position in Kazakhstan and other countries in Asia. While Canaan’s machines are not as energy efficient as Bitmain or MicroBT, in a bull market, this is not as critical and all factored into the price.

Another new ASIC manufacturer has announced it is to enter the space, Intel. The American chip behemoth announced they will be working exclusively with and supplying four companies, Hive Blockchain, Argo Blockchain, Griid Infrastructure and Block (formerly Square). The efficiency of these chips is expected to be 26 joules per terahash (J/TH), according to an Intel announcement. The announcement also says shipments will begin in Q3 of 2022. Producing ASICs is a challenging process and it is very possible the first generation of machines fails to meet expectations. At the same time, only selling to four companies, rather than the more open sales process chosen by the other makers, might not contribute to decentralisation to the extent it could. However, a new entrant like this should be very welcome by the Bitcoin community, it adds considerably to diversity, given the Chinese links of the other three companies and should be a positive for Bitcoin. We have also heard rumours of another large American semiconductor company set to enter the space.

Meanwhile, in Miami MicroBT announced the specification for its new generation of hardware, the 5nm M50 series, with Samsung as the foundry. The new WhatsMiner M50S boasts 126 terahash/second (TH/s) of computing power and efficiency of 26 joules per terahash (J/TH) (The same as Intel). This is 15% more efficient than the M30S++.

Conclusion

With the level of excitement and flow of capital into mining, make no mistake, we are in a raging bull market. This investment in ASIC development and deployment will cause the hashrate to grow at rates faster than many models project. We could be over 320 exahash per second by the end of 2022 (compared to the current rate of 220 exahash per second), even without any significant movement in the Bitcoin price. We are likely to see some listed mining companies fail and many securitised ASIC loans in liquidation. Single digit finance rates could be a thing of the past. Bitcoin mining is not easy and we predict many will learn this the hard way over the next few years. Those that succeed will need to be resilient and think about the long term and not deploy all their capital too quickly.

Ethereum will shortly be switching to proof of stake and almost all new coins are choosing this model. At the same time alternative proof of work coins such as Litecoin, Bitcoin Cash and Ethereum Classic are losing ground. Litecoin, the largest of these coins, is all the way down in 21st position on the coinmarketcap.com table. Proof of work mining is therefore all about one coin, Bitcoin.